Headline SCD Targets:Mapping of Therapeutic Modalities and Pharma Layouts

Another failure in SCD

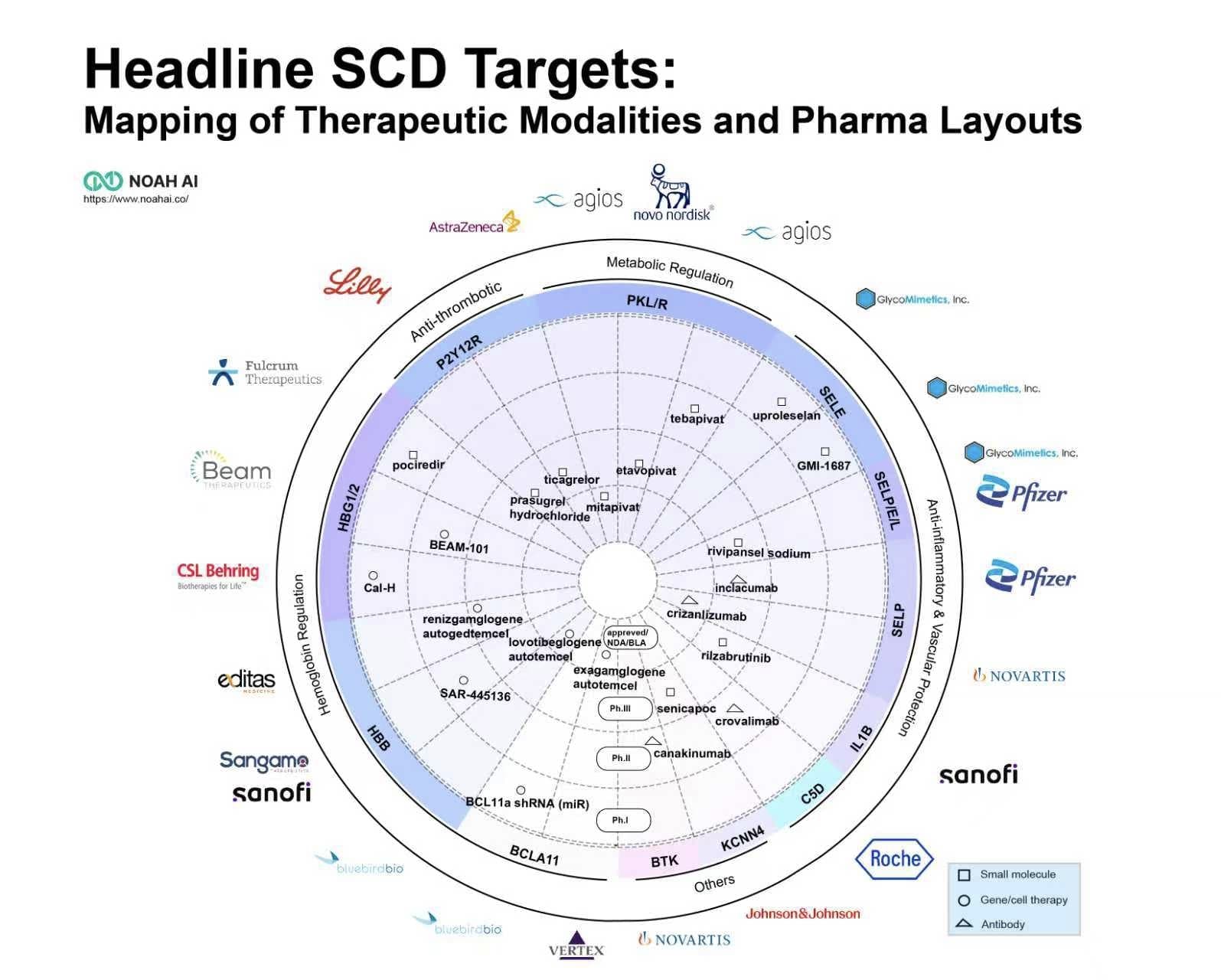

Recently, the field of sickle cell disease (SCD) treatment has witnessed another notable development. On August 15, Pfizer announced that the THRIVE-131 study of inclacumab (PF-07940370) for patients with SCD aged 16 years and older did not meet its primary endpoint. This follows the global market withdrawal of another Pfizer SCD product, Oxbryta (voxelotor), due to safety concerns.

This is not the first setback for the P-selectin target in SCD treatment. Previously, neither Novartis’s Adakveo (crizanlizumab) in the Phase III STAND trial nor Rivipansel, developed by Pfizer and GlycoMimetics, demonstrated satisfactory efficacy in treating vaso-occlusive crises (VOCs) induced by SCD.

P-selectin: How to optimize R&D strategy from a mechanism perspective

These clinical trial failures may be partly attributable to the role of P-selectin in the pathogenesis of VOCs. Research indicates that while P-selectin is a major driver, it is not the sole mechanism. Other inflammatory pathways— such as the formation of neutrophil extracellular traps (NETs)—can precipitate vessel occlusion independently of P-selectin. This helps explain why even successful P-selectin inhibition only reduces VOC events by approximately 50%, rather than preventing them entirely.

Nevertheless, P-selectin remains a validated and important target. Future success may depend on several key factors:

-

Smarter trial design: including standardized endpoint definitions across research centers and the incorporation of composite endpoints alongside validated patient-reported outcomes (PROs) on pain and quality of life.

-

Biomarker-driven patient stratification: such as enrolling individuals with high baseline soluble P-selectin levels or enhanced cellular adhesion, which are predictive of future VOC risk.

-

Advancing combination therapiesthat target the multifaceted pathology of SCD.

The changing SCD therapeutic landscape

Meanwhile, breakthroughs in gene therapy have emerged. The approvals of Casgevy (exagamglogene autotemcel) and Lyfgenia(lovotibeglogene autotemcel) validate core targets such as BCL11A and HBB. However, their adoption faces multiple challenges, including high treatment costs, delays in Medicaid coverage, insufficient reimbursement structures under the framework of DRG, significant logistical barriers for patients, and limited treatment center resources.

Concurrently, research into next-generation small molecule targets—exemplified by PKR—is accelerating. The successful approval of Mitapivat for SCD marks a significant advancement in chronic disease management. The treatment paradigm for SCD is thus evolving toward a dual-track framework: one-time gene therapies aimed at functional cure, and long-term oral small molecule drugs for disease management.

Strategic and Innovative Recommendations by NOAH

R&D and Regulatory Strategy:

-

Design for Confirmation: Even under accelerated pathways, robust Phase III or confirmatory trials should be planned from the outset (referring to the withdrawl of Oxbryta).

-

Leverage Real-World Evidence (RWE): Payers increasingly require RWE to validate trial outcomes. Proactive generation of RWE—such as U.S. Medicaid data showing a 50% reduction in acute care visits with crizanlizumab— may facilitate market access.

-

Innovate in Intellectual Property:The key battleground in gene therapy now lies in manufacturing processes (e.g., scalable electroporation) and safer editing tools (e.g., base editing) to improve the risk-benefit profile.

Market Access and Commercialization:

-

Value-Based Pricing: Outcomes-based agreements are becoming essential for ultra-high-cost therapies. The CMS Cell and Gene Therapy (CGT) Access Model for SCD will likely serve as a template for future launches.

-

Invest in the “Last Mile”: Gene therapy adoption is constrained by treatment center capacity and patient logistics. Investments in qualified treatment center certification, patient navigation, and physician education are critical.

-

Strategic Global Access:While the U.S. remains the primary launch market, hybrid models—combining commercial sales with public-private partnerships, such as Novartis’s initiatives in Sub-Saharan Africa—are essential for reaching patients in high-prevalence, lower-income regions.